Today sees the release of December data from the Ulster Bank Northern Ireland PMI®. The latest report – produced for Ulster Bank by IHS Markit – signalled that the Northern Ireland private sector remained in contraction, but rates of decline in output, new orders and employment all softened. Meanwhile, inflationary pressures strengthened.

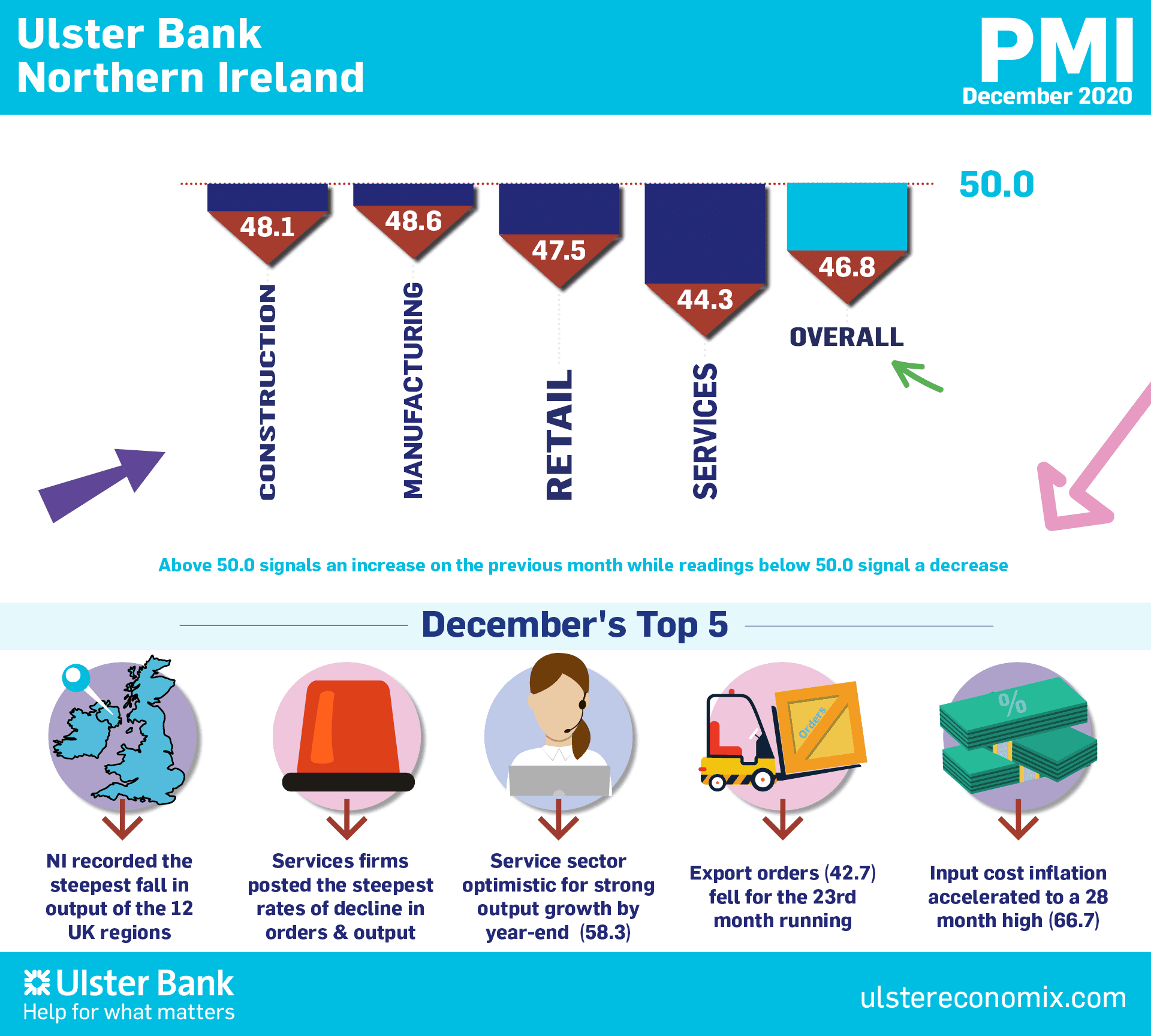

Commenting on the latest survey findings, Richard Ramsey, Chief Economist Northern Ireland, Ulster Bank, said: “Northern Ireland’s private sector ended 2020 the way it began the year with business activity contracting at the same pace in December as in January (46.8). These two months provided a bookend for what was a dramatic year for economies worldwide.

Commenting on the latest survey findings, Richard Ramsey, Chief Economist Northern Ireland, Ulster Bank, said: “Northern Ireland’s private sector ended 2020 the way it began the year with business activity contracting at the same pace in December as in January (46.8). These two months provided a bookend for what was a dramatic year for economies worldwide.

“Economic forecasts made a year ago proved to be so wide of the mark that they quickly became meaningless. The local economy experienced six months of contraction during the first half of 2020, including the record rates of decline across a range of indicators in the second quarter. Indeed some of the PMI indicators hit single-digits, a feat that was unheard of prior to the pandemic and the use of lockdowns. A robust rebound occurred in the third quarter with three months of output growth.

“However, this recovery was short-lived and faltered as renewed lockdown restrictions triggered three months of contraction during the final quarter of the year.

“December’s PMI survey smacked of déjà vu with all four sectors posting declines in both output and employment; like most of 2020. Meanwhile export orders notched up their twenty-third successive month of decline.

“The one area where growth is accelerating is inflation. Input costs rose at their fastest pace since August 2018 with inflationary pressures most marked amongst manufacturers. In turn, firms are passing on these higher costs, such as freight and raw materials, to their customers. As a result, the selling prices of goods and services are rising at their fastest rate in almost two years.

“Services was the sector where firms posted the fastest rates of decline in output and new orders – not only in December but for 2020 as a whole. This contrasts with previous recessions whereby services has traditionally been the least affected sector.

“Services remains the only sector not to experience a pick-up in new orders since the first lockdown. However, more encouragingly, services firms did report a surge in business confidence in December with optimism surrounding the 12-month outlook at its highest level since February 2020.

“The arrival of a number of vaccines has already provided a general boost to business confidence. Furthermore, the recent UK-EU trade deal (secured after this survey was conducted) has taken the risk and uncertainty of a ‘no-deal’ Brexit off the table.

“This will act as an additional boost to confidence for 2021. In the meantime, however, we can expect teething problems to emerge as firms on both sides of the Irish Sea get to grips with the new trading arrangements. Even when these are mastered the reality is that trade will be more restricted, involve more bureaucracy, and therefore be more costly than before. Following last year’s salutary lesson, economic forecasters will this year be wary of making predictions for the 12 months ahead. But it looks like the speed and scale of the vaccine rollout will be the biggest and most important factor determining economic performance in 2021.”

The main findings of the December survey

The headline seasonally adjusted Business Activity Index posted 46.8 in December, up from 45.6 in November but signalling a reduction in business activity for the third month running. Respondents indicated that the coronavirus disease 2019 (COVID-19) pandemic was the principal cause of the latest fall. A similar picture to activity was seen with regards to new orders, which decreased in December but at a softer pace.

Although employment continued to fall in December, the rate of job cuts eased to the weakest in the current ten-month sequence of decline. Input costs increased at the fastest pace since August 2018, often due to higher raw material prices but also reflecting rising shipping costs amid widespread issues with freight. Inflationary pressures were particularly strong at manufacturers.

The passing on of rising input costs to customers resulted in a marked increase in selling prices. Companies remained optimistic, with sentiment at its highest since February.