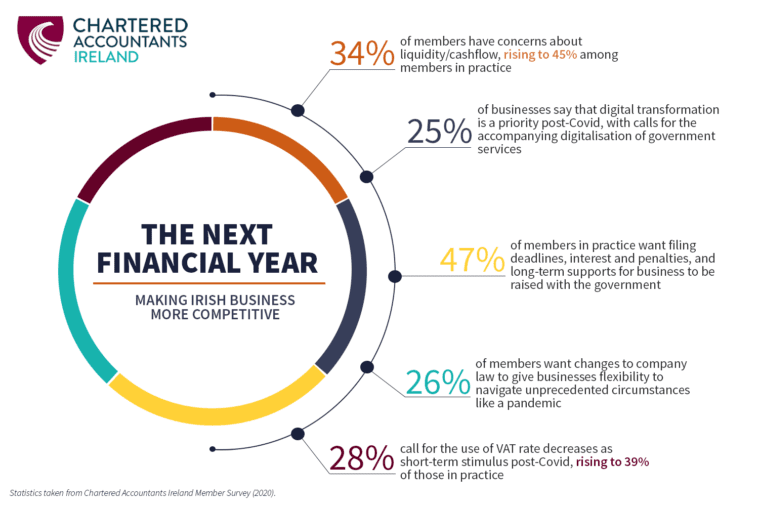

Liquidity and cash flow are key concerns for one-third of businesses in a post-Covid economy according to new data released today by Chartered Accountants Ireland from almost 2,000 members surveyed by the Institute on the island of Ireland.

With almost a third of Northern Ireland respondents reporting a need to overhaul their business model post-pandemic, businesses, in particular SMEs, have highlighted specific measures that can help in the period ahead, including:

- More than a third called for greater accessibility of business loans, grants and reliefs

- Almost half of those working in practice called for greater leniency on filing deadlines, interest and penalties

- Digital transformation is a priority for 1 in 4 businesses post-Covid, with calls for an accompanying full digitalisation of government services

- Longer term business supports post-Covid and the use of VAT rate decreases as short-term stimulus were raised by 28 percent of members, rising to 39 percent of those in practice.

The findings are released as the Institute publishes “The Next Financial Year: Making Irish Business More Competitive”, a new position paper which identifies pathways to a better business environment in and after the pandemic. Informed by extensive engagement with members working in practice, industry, SMEs and the public sector, the paper sets out proposals to create workable solutions and alternatives across a range of areas, including digitalisation, tax measures and business supports now open to government / policymakers to consider. [Details below]

Commenting, Dr Brian Keegan, Director of Public Policy, Chartered Accountants Ireland said “SMEs are fighting to stay afloat and post-pandemic, many will reimagine how they function or will pivot into new activities. Supports are currently based on the way that business has always been done, but with this changing, “The Next Financial Year” outlines a simplified, more flexible approach.

“Now is not the time to rely on dogged and uncommercial approaches. Government policy must be focussed on providing maximum support and flexibility to businesses.”

Liquidity and cash flow

The proposals include an emphasis on digitalisation and ensuring government services and supports keep pace with changing business models post-pandemic, and the realities of operating as an SME at this time. These include: –

Digitalisation

Remote working has been one of the most visible signs of change since March. Many workers are now trusted to work productively from home where possible; and it is now acceptable to hold significant business meetings online. Chartered Accountants Ireland calls for the momentum to be maintained by increased support for the education and adoption of digital competencies across the business community through increased grant-funded programmes.

Government must also play its part in supporting digitalisation, namely:

- further enabling by HMRC of online filing mechanisms, for example inheritance tax (IHT), Forms IHT 100 and 400, and the retention of such mechanisms on a permanent basis,

- resourcing of HMRC to develop new digital services as effective as the job retention and self-employed income support online portals,

- extend the availability of the Coronavirus Business Interruption Loan Schemes for at least a further six months,

- closely review the resourcing of HMRC to ensure the department can deal with EU-exit queries, ‘business as usual’ in the tax system and the ongoing Covid-19 supports.

Other key proposals include

- early access to corporate trading losses: temporary targeted measures to enable early access to Covid-19 related losses,

- delay by two years the commencement of the amendment relating to the protection of tax in an insolvency, until the Covid-19 schemes have reached completion,

- a temporary doubling to £10 million of the deductions allowance for losses carried forward for a two-year period from 1 April 2021,

- a three-month suspension to the imposition of late filing and payment penalties for 2019/20 self-assessment returns,

- a similar suspension in respect of late-filing penalties for company tax returns due for filing between March 2020 and April 2021,

- suspend interest on underpayments on 2020/2021 payments on account under the self-assessment regime,

- consider introducing warehousing measures for both VAT and PAYE – any warehousing arrangements introduced should also cover corporation tax.